2025-10-04

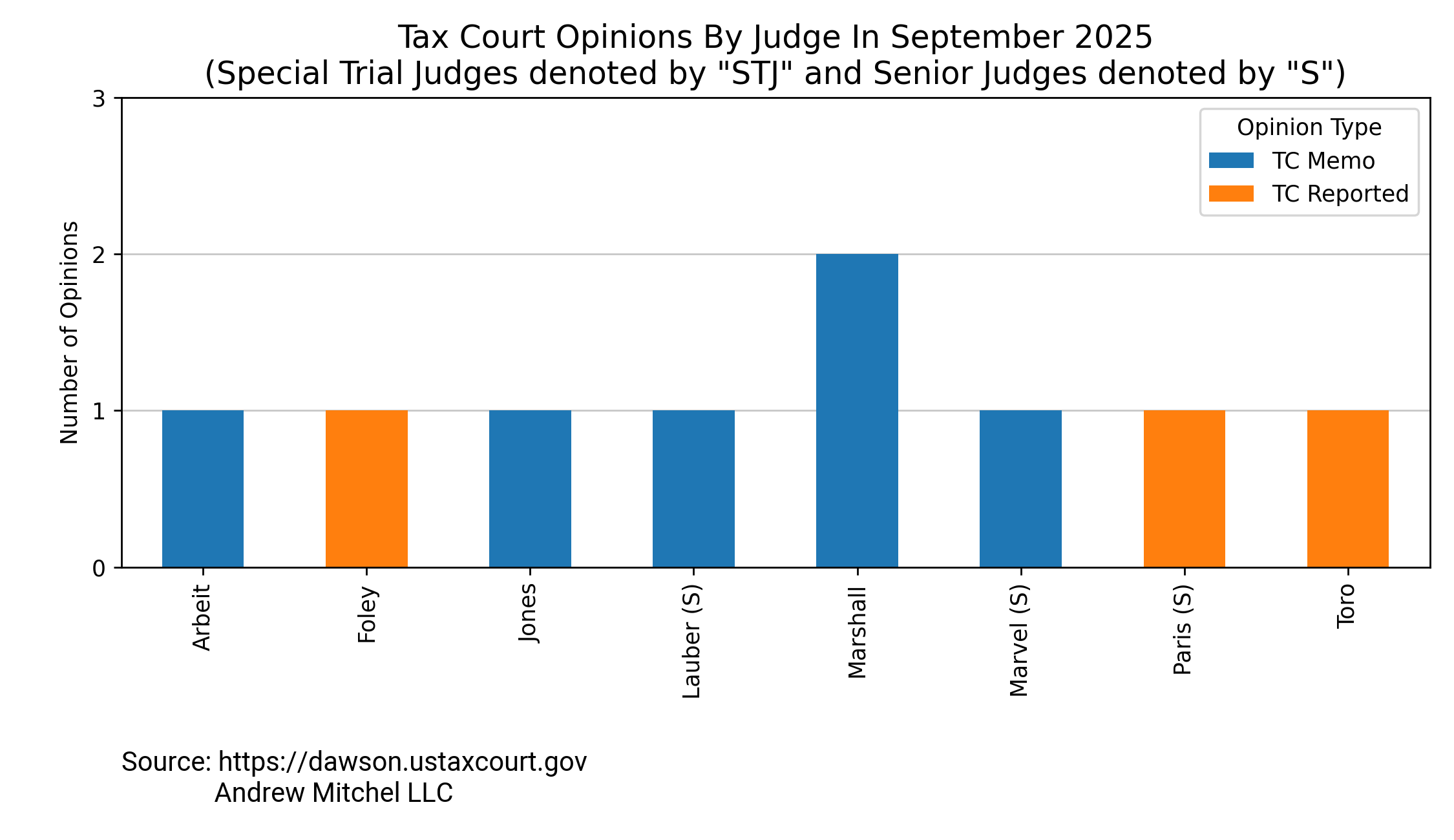

In September 2025, the Tax Court published 9 opinions, which included a total of 362 pages. Below are graphs for the month showing: (i) the top 15 code sections referenced, (ii) cases cited 5 or more times, (iii) the number of opinions by judge, and (iv) the number of pages by judge.

I am always interested in learning well-established tax principles. Often, court cases will explicitly indicate that a tax principle is well established or well settled. Or the court may concisely state the holding of a prior case in a parenthetical. Below are excerpts from the September 2025 Tax Court cases referring to these types of principles or holdings.

Fumo v. Commr., T.C. Memo. 2025-97. (Lauber)

"Under the constructive receipt doctrine 'funds [or other property] which are subject to a taxpayer's unfettered command and which he is free to enjoy at his option are constructively received by him whether he sees fit to enjoy them or not.'" Estate of Caan v. Commissioner, 161 T.C. 77, 95 (2023) (alteration in original) (quoting Estate of Brooks v. Commissioner, 50 T.C. 585, 592 (1968))

Fumo v. Commr., T.C. Memo. 2025-97. (Lauber)

Murphy v. United States, 992 F.2d 929, 931 (9th Cir. 1993) (holding that a taxpayer constructively received income where "his failure to receive cash was entirely due to his own volition")

Fumo v. Commr., T.C. Memo. 2025-97. (Lauber)

Estate of Geiger v. Commissioner, 352 F.2d at 231-32 (finding that taxpayer had constructive receipt of income where she was the "force and the fulcrum" behind the misappropriations)

Fumo v. Commr., T.C. Memo. 2025-97. (Lauber)

Leslie v. Commissioner, T.C. Memo. 2016-171, 112 T.C.M. (CCH) 313, 318 (finding that a substantial limitation existed where the taxpayer's access to funds required a court order to release the money)

Fumo v. Commr., T.C. Memo. 2025-97. (Lauber)

Walters v. Commissioner, T.C. Memo. 1998-111, 75 T.C.M. (CCH) 2007, 2018-19 ("[A]n embezzler must include embezzled funds in income even though the funds are lent or given to another.")

Fumo v. Commr., T.C. Memo. 2025-97. (Lauber)

Estate of Geiger v. Commissioner, 352 F.2d at 231 ("Income . . . is not restricted to cold cash in a taxpayer's fist.")

Fumo v. Commr., T.C. Memo. 2025-97. (Lauber)

Hornung v. Commissioner, 47 T.C. 428, 437, 440 (1967) (finding that the taxpayer's "free use" of two Ford Thunderbird convertibles constituted gross income)

Fumo v. Commr., T.C. Memo. 2025-97. (Lauber)

Treas. Reg. § 1.61-1(a) ("Gross income includes income realized in any form, whether in money, property, or services.")

Fumo v. Commr., T.C. Memo. 2025-97. (Lauber)

But the law is well established that a person is taxable, not only on property he receives himself, but on the value of property he causes to be diverted to the objects of his bounty.

Fumo v. Commr., T.C. Memo. 2025-97. (Lauber)

Badaracco v. Commissioner, 464 U.S. 386, 394 (1984) (holding that the filing of a proper amended return does not purge the fraud evidenced by the filing of a fraudulent original return)

Fumo v. Commr., T.C. Memo. 2025-97. (Lauber)

Meier v. Commissioner, 91 T.C. 273, 302 (1988) (holding that a taxpayer's inadequate recordkeeping evidenced an intent "to conceal information" from the IRS)

Gottesman v. Commr., T.C. Memo. 2025-94. (Jones)

Adams v. Commissioner, 122 F.4th 429, 433 (D.C. Cir. 2024) ("The D.C. Circuit is the default venue for appeals of Tax Court decisions.")

Gottesman v. Commr., T.C. Memo. 2025-94. (Jones)

Estate of Israel v. Commissioner, 159 F.3d 593, 595 (D.C. Cir. 1998) (holding that D.C. Circuit was proper venue where one taxpayer's legal residence was Bermuda)

Gottesman v. Commr., T.C. Memo. 2025-94. (Jones)

Castillo v. Commissioner, 84 T.C. 405, 408 (1985) ("The burden of proving fraud is on [the Commissioner], and he must do so by clear and convincing evidence.")

Gottesman v. Commr., T.C. Memo. 2025-94. (Jones)

Voccola v. Commissioner, T.C. Memo. 2009-11 (observing that the Commissioner can satisfy his burden of proof as to section 6663 fraud penalties by deemed admissions)

Gottesman v. Commr., T.C. Memo. 2025-94. (Jones)

United States v. Bodwell, 66 F.3d 1000, 1001-02 (9th Cir. 1995) (stating that the only way the Fifth Amendment can be asserted as to testimony is on a question-by-question basis)

Moon v. Commr., 165 T.C. No. 4 (2025). (Foley)

Consumers Power Co. v. Commissioner, 89 T.C. 710, 724 (1987) (holding that a hydroelectric power plant was placed in service only once it had passed all required inspections and was regularly generating power)

Moon v. Commr., 165 T.C. No. 4 (2025). (Foley)

Madison Newspapers, Inc. v. Commissioner, 47 T.C. 630, 637 (1967) (holding that a printing press was placed in service when the unit was installed and regularly publishing newspapers)

Savage v. Commr., 165 T.C. No. 5 (2025). (Toro)

In Patients Mutual Assistance Collective Corp. v. Commissioner, 151 T.C. 176, 198-99 (2018), aff'd, 995 F.3d 671 (9th Cir. 2021), we held that a single taxpayer could have multiple trades or businesses, some of which would be subject to section 280E and some of which would not, or a single trade or business consisting of multiple activities all of which would be subject to section 280E, even if the activities are undertaken through separate entities.

Savage v. Commr., 165 T.C. No. 5 (2025). (Toro)

United Therapeutics Corp. v. Commissioner, 160 T.C. 491, 513 (2023) (explaining that a cardinal principle of interpretation requires that we give effect, if possible, to every clause and word of the statute and collecting authorities)

Savage v. Commr., 165 T.C. No. 5 (2025). (Toro)

K Mart Corp. v. Cartier, Inc., 486 U.S. 281, 291 (1988) ("In ascertaining the plain meaning of the statute, the court must look to the particular statutory language at issue, as well as the language and design of the statute as a whole.")

Supinger v. Commr., T.C. Memo. 2025-93. (Marshall)

Cabirac v. Commissioner, 120 T.C. 163, 169 (2003) (holding that filing a zero return does not constitute an honest and reasonable attempt to supply the information required by the Code)

Supinger v. Commr., T.C. Memo. 2025-93. (Marshall)

Reiff v. Commissioner, 77 T.C. 1169, 1177-78 (1981) (holding that filed zero return did not constitute a valid return because it did not contain sufficient data from which the IRS could compute and assess taxpayer's income tax liability)

Supinger v. Commr., T.C. Memo. 2025-93. (Marshall)

Richmond v. Commissioner, T.C. Memo. 2011-251 (holding that taxpayer's zero return did not contain "sufficient data to calculate a tax liability" and did not constitute "an honest and reasonable attempt to satisfy the requirements of the tax law")

Young v. Commr., T.C. Memo. 2025-95. (Marvel)

Gitlitz v. Commissioner, 531 U.S. 206, 209 (2001) ("Subchapter S allows shareholders of qualified corporations to elect a 'pass-through' taxation system under which income is subjected to only one level of taxation.")

Young v. Commr., T.C. Memo. 2025-95. (Marvel)

Hotel Kingkade v. Commissioner, 180 F.2d 310, 312 (10th Cir. 1950) ("Generally, an expenditure should be treated as of a capital nature if it brings about the acquisition of an asset having a period of useful life in excess of one year or if it secures a like advantage to the taxpayer which has a life of more than one year.")

Young v. Commr., T.C. Memo. 2025-95. (Marvel)

Jackson v. Commissioner, 59 T.C. 312, 317 (1972) ("[S]uffering has never been made a prerequisite to deductibility.")

Young v. Commr., T.C. Memo. 2025-95. (Marvel)

Flume v. Commissioner, T.C. Memo. 2020-80, at *37 ("Simply employing a tax return preparer for the years at issue does not permit [the taxpayers] to avoid accuracy-related penalties.")

In September 2025, the IRS published 9 Announcements, Notices, Revenue Procedures, and Revenue Rulings, which included a total of 246 pages.

In September 2025, the IRS published 114 Written Determinations, which included a total of 649 pages.